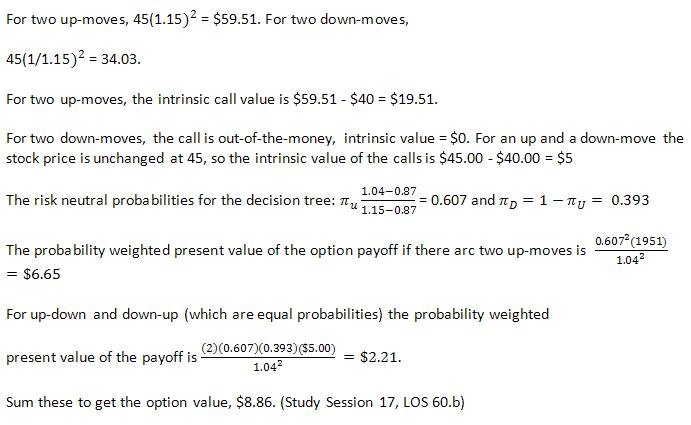

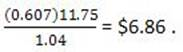

Michelle Norris, CFA, manages assets for individual investors in the United States as well as in other countries. Norris limits the scope of her practice to equity securities traded on U .S . stock exchanges. Her partner, John Witkowski, handles any requests for international securities. Recently, one of Norris's wealthiest clients suffered a substantial decline in the value of his international portfolio. Worried that his U .S . allocation might suffer the same fate, he has asked Norris to implement a hedge on his portfolio. Norris has agreed to her client's request and is currently in the process of evaluating several futures contracts. Her primary interest is in a futures contract on a broad equity index that will expire 240 days from today. The closing price as of yesterday, January 17, for the equity index was 1,050. The expected dividends from the index yield 2% (continuously compounded annual rate). The effective annual risk-free rate is 4.0811%, and the term structure is flat. Norris decides that this equity index futures contract is the appropriate hedge for her client's portfolio and enters into the contract.

Upon entering into the contract, Norris makes the following comment to her client:

"You should note that since we have taken a short position in the futures contract, the price we will receive for selling the equity index in 240 days will be reduced by the convenience yield associated with having a long position in the underlying asset. If there were no cash flows associated with the underlying asset, the price would be higher. Additionally, you should note that if we had entered into a forward contract with the same terms, the contract price would most likely have been lower but we would have increased the credit risk exposure of the portfolio."

Sixty days after entering into the futures contract, the equity index reached a level of 1,015. The futures contract that Norris purchased is now trading on the Chicago Mercantile Exchange for a price of 1,035. Interest rates have not changed. After performing some calculations, Norris calls her client to let him know of an arbitrage opportunity related to his futures position. Over the phone, Norris makes the following comments to her client:

"We have an excellent opportunity to earn a riskless profit by engaging in arbitrage using the equity index, risk-free assets, and futures contracts. My recommended strategy is as follows: We should sell the equity index short, buy the futures contract, and pay any dividends occurring over the life of the contract. By pursuing this strategy, we can generate profits for your portfolio without incurring any risk."

Sixty days after the inception of the futures contract on the equity index, Norris has suggested an arbitrage strategy. Evaluate the appropriateness of the strategy. The strategy is: